Kinsale FY23 Results

Great execution, and strong outlook for FY24

Ticker: KNSL 0.00%↑

Market Cap: $11.7 billion

Price: $505.03 (16 Feb 2024)

How did Kinsale do in FY2023?

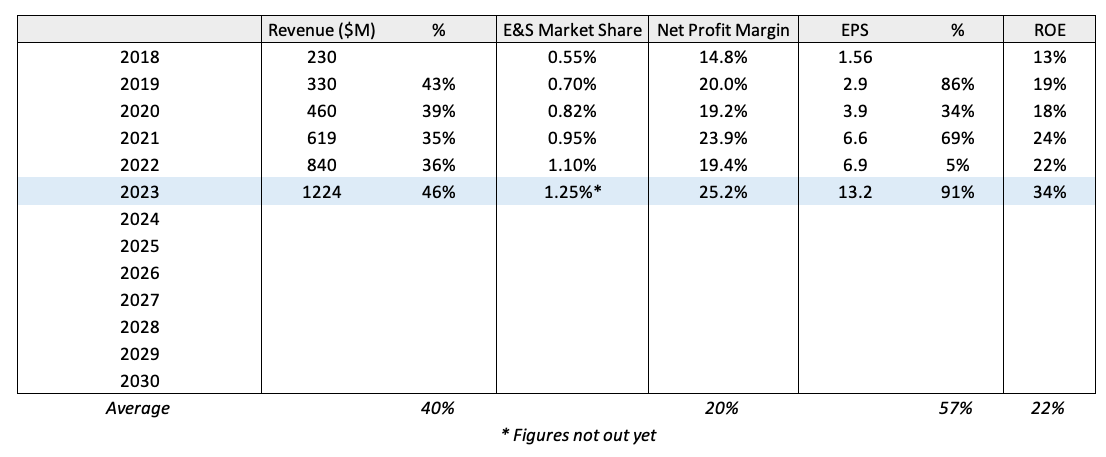

Kinsale posted great Q4 results yesterday, beating expectations on both revenue and earnings. Shares traded +16%, a huge daily move for the company relative to its usual volatility. It has fully recovered from its drawdown back in November and is trading at a new ATH of $505.

Looking at the how Kinsale performed in FY23, it has delivered on all cylinders:

+46% Revenue (YoY)

+91% Diluted EPS Growth (YoY)

ROE improved to 34% vs 22%

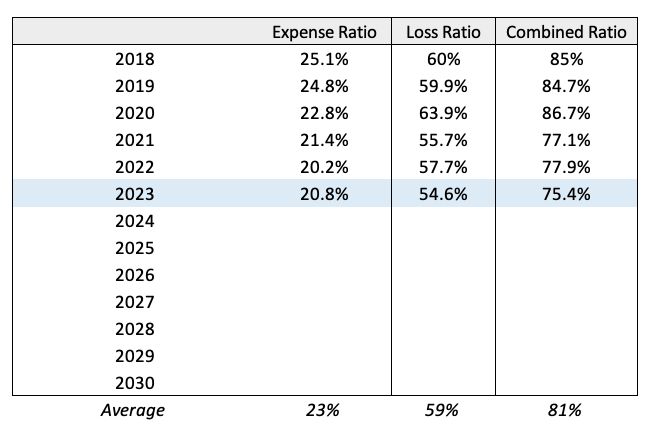

Expense ratio maintained around 21%, loss ratio dropped by 3%, combined ratio improved to 75.4% from 77.9%

Kinsale continues to ride the wave of the hot E&S market, with an inflow of business from clients who cannot get covered by standard insurers and rate increases driven by inflation and a relatively tight underwriting conditions.

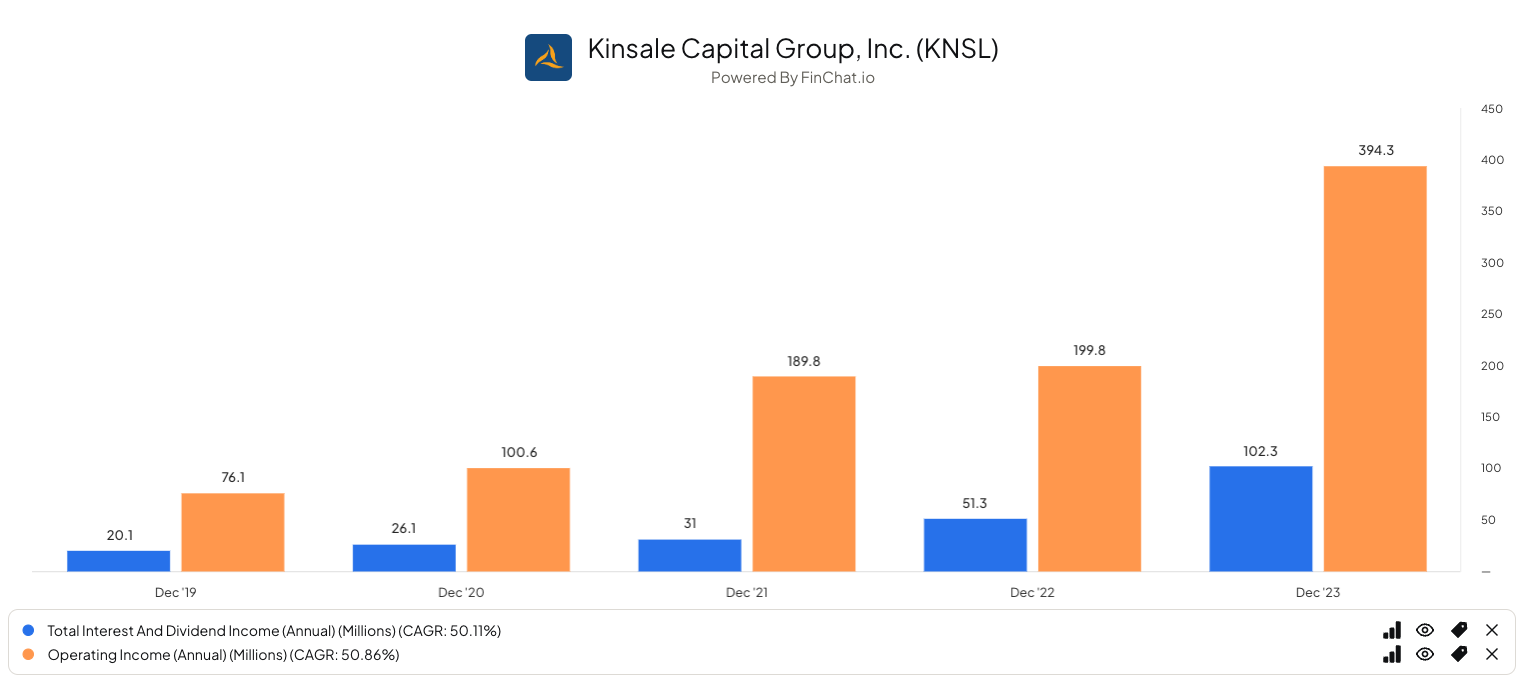

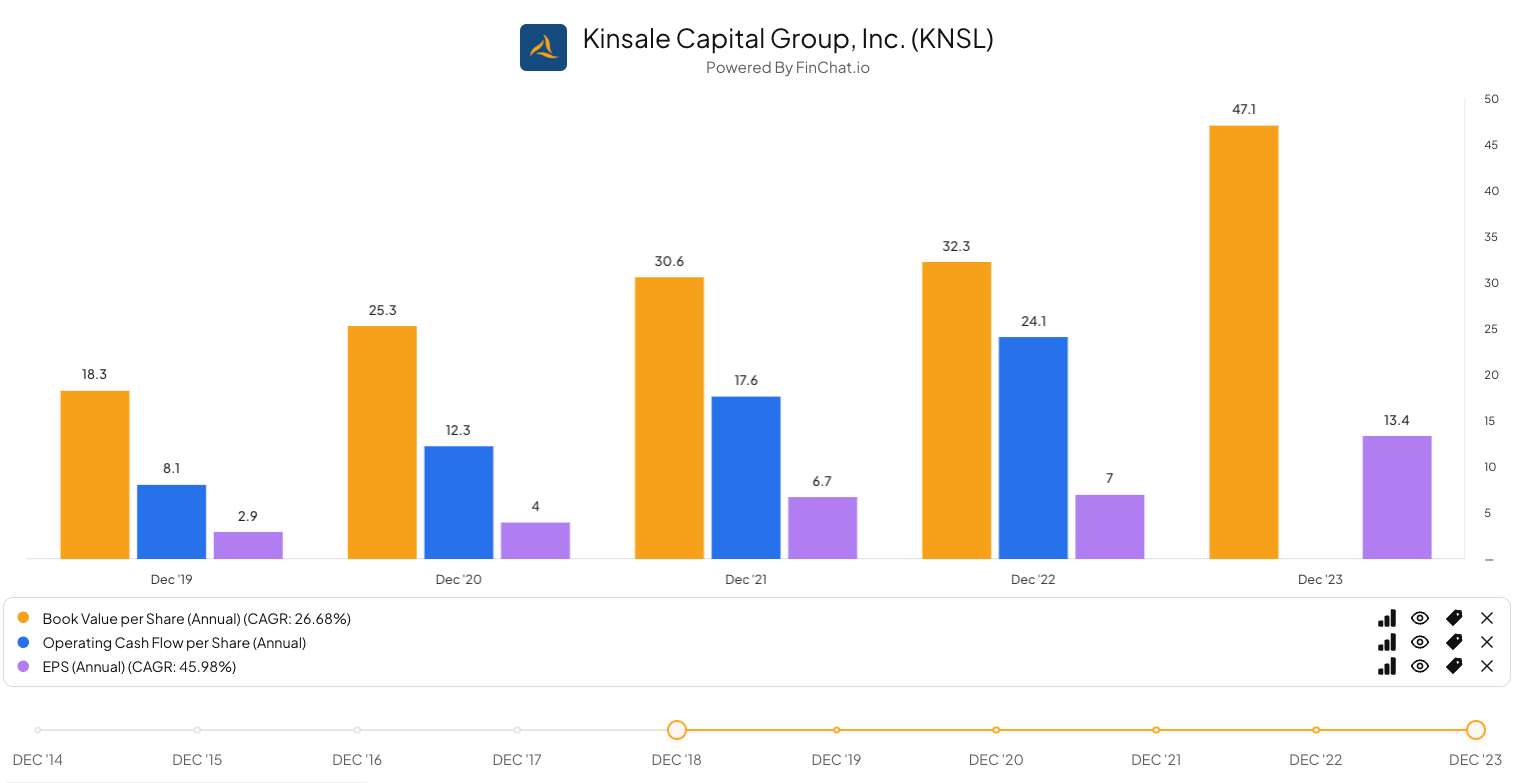

Kinsale’s Financials (2018 - 2023)

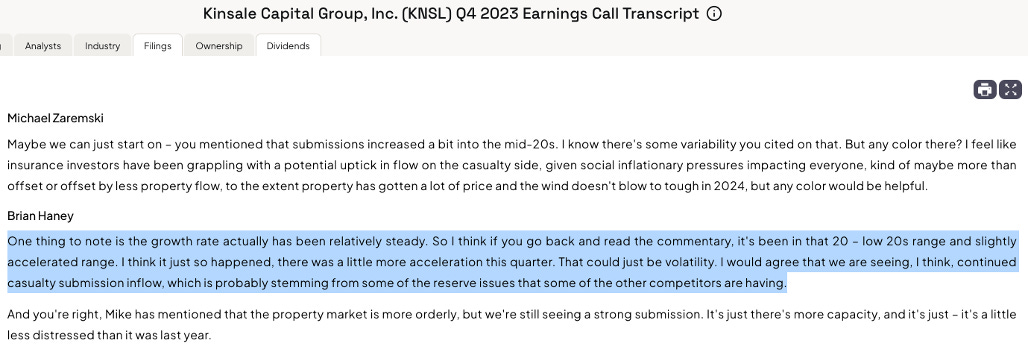

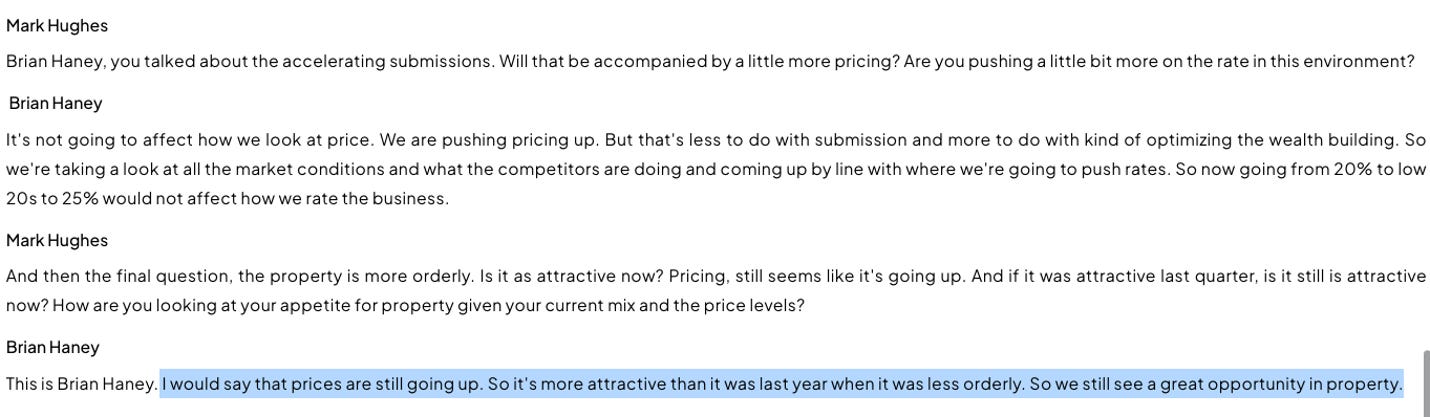

Snips from Q4 earnings call transcript I found interesting

Tone by management is much more positive this call, quoting a re-acceleration in submission growth (volume) and rates (pricing) across the different divisions.

Areas to improve in 2024?

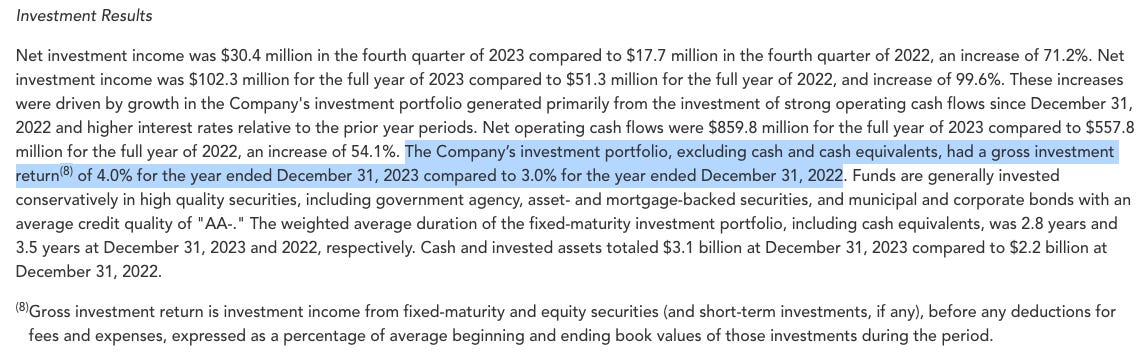

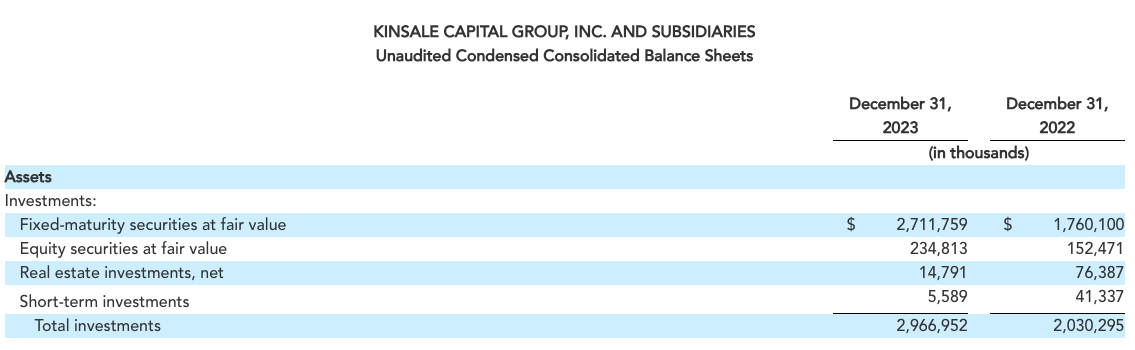

One thing to note is that Kinsale currently reinvests almost all its retained earnings into government treasuries. In the long run, this will have a diluting effect on ROE% as underwriting earnings growth will be blended with the lower investment returns from T-bills. While this strategy doesn’t look as bad in a high interest rate environment, it will start to show cracks as interest rate trends down.

It will be very interesting to see how Kinsale manages its investment float especially as it becomes a larger player like Progressive/GEICO where investment returns from float > underwriting earnings.

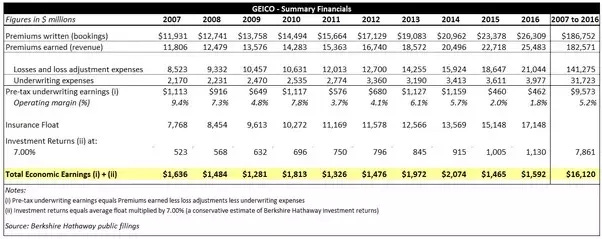

Currently, investment income makes up only 25% of Kinsale’s earnings while underwriting earnings makes up 75%. Take a look below at GEICO’s income statement: Investment/Underwriting income split became closer to 50%/50% or even 66%/33% on bad years.

This is a critical function and value driver for Kinsale that it needs to spend more effort on. I hope to see Michael address this in the upcoming earning calls.

This is of course a problem for the future. For now, I find comfort that Kinsale is using the past few good years to build up resiliency in its balance sheet for tougher times (eg. higher CAT activity) and softer market conditions.

Then again, if the book value grow really fast - it is a good problem as that means Kinsale is incredibly cash flow generative.

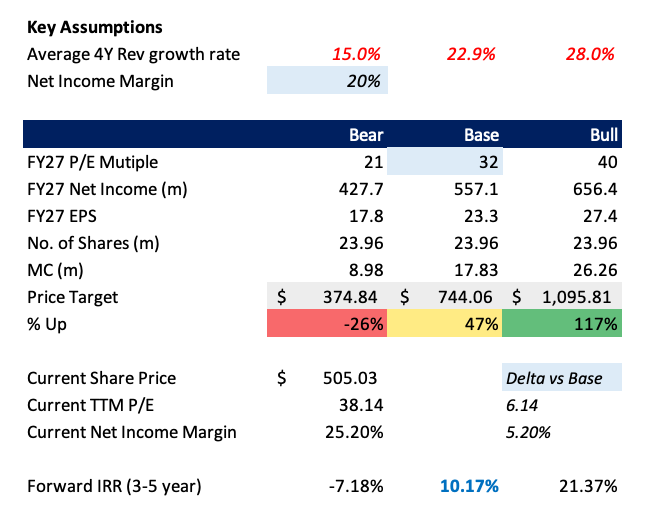

Valuation

Kinsale has since traded up by 50% from my first post. Even though it has moved up so quickly over the past 2 months, I am comfortable with holding onto my shares.

I believe my base case to be very achievable for Kinsale as it factors in:

1) Lower net margin 20%

2) P/E multiple of 32 (lower-end of P/E range)The outlook for FY24 is still looking promising for E&S market with more standard lines moving over to the E&S market and a strong pricing environment. If Kinsale continues to deliver closer to 25-30% EPS growth in FY24, I believe we will see prices move closer towards the bull case, especially if multiples revert back to the 40-50x range

If multiples stay at current levels, I believe fair price is around 10% higher from current levels by the end of the year - assuming that it delivers 23% top line growth.

“The real key to making money in stocks is not to get scared out of them.”

Peter Lynch

I have to constantly remind myself of this.

If you enjoyed this article, make sure you’re subscribed here on substack so you don’t miss future content. Consider following me on Twitter as well @limhongyu, where I post timely market-related content on my portfolio holding