Part 1: Altus Power ($AMPS)

Part 1: Altus Power ($AMPS)

A pure-play clean electrification producer with a massive pipeline of untapped commercial & industrial tenants (Blackstone and CBRE)

Ticker: AMPS 0.00%↑

Market Cap: $1.35 billion

Price: $8.41 (17 Jan 2023)

Executive Summary

Altus Power is currently the only pure-play clean electrification stock in the commercial and industrial (C&I) segment. With an evolving demand for clean electricity, AMPS is in a sweet spot to capitalize on the growth of the C&I segment which accounts for 50% of the total electricity demand in the US in a $400b/year market.

Penetration rate of C&I with solar rooftops installed is currently sitting at 5%. Altus is poised to capitalize on the transition from traditional fossil-fuel generated electricity towards PV-powered electricity in the C&I space.

Altus has strategic partnership with 2 of the largest real estate managers in the world (Blackstone and CBRE), unlocking access to financing at cheaper costs and a steady pipeline of C&I tenants both in the US and internationally.

Part I will cover the business model and why I like the company

Part II will go over how the stock fits my investment checklist and identify any key risks to watch out for.

Business Model

Altus builds, own and operates solar panels on commercial and industrial rooftops, carparks and surrounding land. They sell the power generated to commercial or retail customers through long term contracts. On top of that, it also operates energy storage systems along with EV charging facilities, serving both commercial and industrial, public sector, and community solar customers.

The model is a win win for the users/tenant and the landlord (Blackstone & CBRE) as customers enjoy cost savings and landlords earn additional rental income on rooftop/carparks that would have otherwise have been left idle.

It currently operates only in the US, with majority of their installations in Massachusetts, New Jersey, Minnesota, and Hawaii.

Why I like them

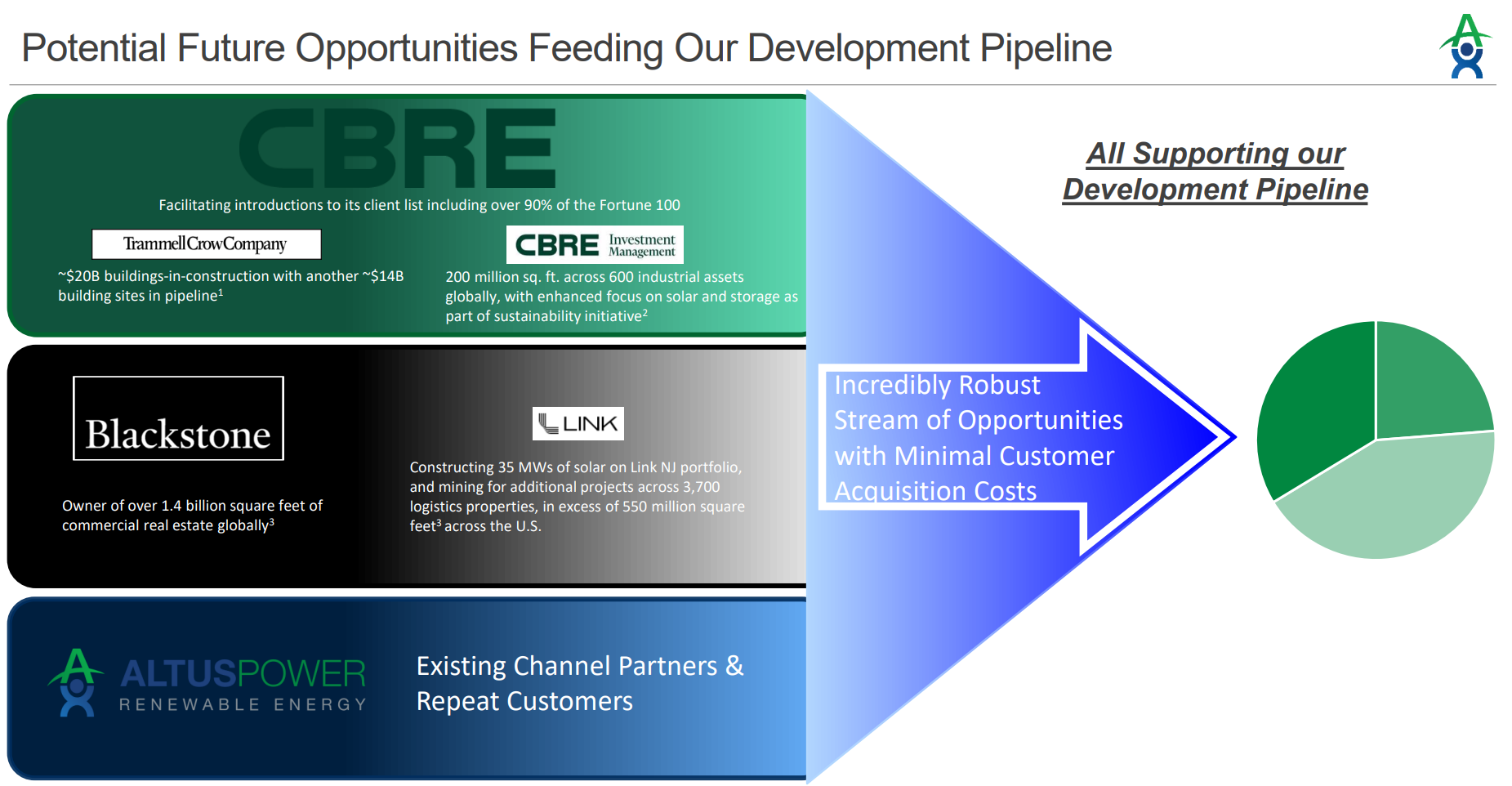

1. Strategic partnership with Blackstone and CBRE (Largest real estate owners)

Due to favourable partnership with CBRE and Blackstone - they have a stable pipeline of commercial tenants waiting to onboard which allows them to grow their generation capacity at minimal customer acquisition costs. This partnership is their competitive advantage over other competitors that allow higher operating margins.

They have access to Blackstone's (BX) credit facility, which provides access to financing at a cost of capital that is among the lowest in the industry.

2. Durable top-line growth with stable recurring B2B revenue

Altus operates in a space that is resilient in any macro conditions due to the nature that electricity demand is a necessity, regardless of the economic conditions.

The service provided is also recurring in nature with low churn as tenants usually sign a 20 year tenant contract - creating a predictable base cashflow.

3. Optionality for new revenue streams on top of selling power on an as-generated basis from the solar assets

Cross-selling new products: With long duration contracts with their customers (>20 years) it allows them to cross-sell additional present and future products and services - eg. charging station for carpark charging, selling excess power to the grid, marketing of carbon offsets etc.

International Expansion: Blackstone has commercial real estate globally so scaling into markets outside of the US is not difficult - plug and play

Licensing: AMPS has developed a proprietary software Gaia that provides and end-to-end fully-integrated platform to enable asset management throughout the development and operations lifecycles which can be licensed to other solar providers or users who want to DIY their electricity generation

4. Shareholder Ownership Alignment

30% owned by CBRE and Blackstone - It is in their incentive to keep supporting Altus’s growth - be it with new tenants or cheap cost of capital for acquiring/building new generation capacity.

40% owned by founders - Extremely high ownership, founder-led - They want the company to do well even more than me…..

30% owned by public