Part 2: Altus Power ($AMPS)

Part 2: Altus Power ($AMPS)

A pure-play clean electrification producer with a massive pipeline of untapped commercial & industrial tenants (Blackstone and CBRE)

Scorecard: 7 out of 9

1. Market Cap - Does it have a small market cap relative to terminal market cap?

✓

AMPS is currently at a 1.3b market cap with 100m~ of LTM revenue.

$400 billion is spent on electricity yearly, of which 50% is spent on C&I. According to a 2020 WoodMac Report, the penetration rate for C&I rooftops that uses solar power is only at 5%, with installed C&I solar capacity is predicted to grow at approximately 12% per annum from 2020 to 2050. With increasing customer demand for making the switch to renewable energy and increased battery storage demand, the secular trend is intact for sustained topline growth as more C&I users make the switch.

Assuming Altus takes 1-5% of the C&I electricity spend annually, Altus will be grossing somewhere between 2b - 10b of sales annually. With a 20% FCF margin, this will land us somewhere between $400m-$2b in cashflow annually. Assuming a terminal EV/FCF of 10 - 15, Altus power should be able to achieve a market cap of $4-30b market cap, which gives an upside of 3x - 23x from current valuations.

Largest US renewable energy companies in the US by Market Cap

2. Mission-critical and sticky service/product

Product/Service that is very much needed for society and something where customer would become much less productive or not be able to function without it + high switching costs. This makes the product demand price inelastic where it raises prices without churning customers (eg. Microsoft Office, AWS)

✓

Value proposition makes sense commercially to both users - the tenants and landlords as they benefit from discounted energy price and added rental revenue.

In terms of stickiness, once a tenant is locked up for a 20 year contract, as electricity is not a huge % of the running business cost so they will usually find little incentive to switch to a competitor unless there is significant cost savings. Hence, customer churn is less likely than other industries.

3. Growth Runway

Where do you see the company’s revenue 5-10 years from now. Can it consistently grow revenue at >20% a year - most of the times the company must operate in an industry that is consumer facing and build a brand to achieve this. Is their service/product something that is part of a secular growth trend with massive TAM potential??? Is there optionality to spawn new business segments that allow for new growth drivers within the company??

eg. Apple who started from one product and kept coming up with new product lines.

✓

My personal expectation is for them to grow top line at an average range of 30% annually within the next 5- 7 years, before slowing down to the 10 - 20% range due to the physical limitations as it takes time to acquire/construct more generation capacity and it is harder to grow as fast in % terms when their top line is starting from a larger base.

I see a lot of optionality for Altus to increase the velocity of its revenue growth

Cross-selling new products: With long duration contracts with their customers (>20 years) it allows them to cross-sell additional present and future products and services - eg. charging station for carpark charging, selling excess power to the grid, marketing of carbon offsets etc.

International Expansion: Blackstone has commercial real estate globally so scaling into markets outside of the US is not difficult - plug and play

Community Solar: By using C&I scale generated solar and selling it to retail at retail prices you have the best unit economics vs a pure retail solar installer. Altus could set the playing field for the future as brown power phases out to green power.

Licensing: AMPS has developed a proprietary software AltusIQ that provides and end-to-end fully-integrated platform to enable asset management throughout the development and operations lifecycles which can be licensed to other solar providers or users who want to DIY their electricity generation

4. Business Economics - Margins

Is this business operating in an industry where operating margins are worthwhile (>20%) when it mature?? (Think Mastercard, SPGI, MCO) How does the company GP margin stack up againts its competitors? (This demonstrates competitive advantage) Gross margin is much more difficult to fix than operating margins as it is easier to trim OPEX than COGS in the long run.

✓

I expect EBITDA margins to remain high 50% to low 60% for the foreseeable future, especially since their cost of debt for the construction of these assets are securitised and syndicated to Blackstone insurance on a 25 year basis, which locks in the margin and reduces refinancing risk. Every $1 of revenue brings in around $0.40 of operating cashflow which allows it to fund further growth.

At scale, this will be operating at a 10-20% FCF margin once its asset portfolio matures which is very decent, especially since its earnings are very durable with customers on 20 year contracts.

Potential risks would be if prices power drops with increased power supply green + brown such that $/KWh drops. >50% of the customers opt for floating price, which means margins could compress if the long term trend is pointing towards cheaper power prices sold to customers. However, this works in Altus’s favour if power prices picks up as electricity demand increases faster than supply, which is very possible as electrification of transportation vehicles continues to grow from cars, busses, trucks etc.

5. Operating Leverage

Can the operating margins improve over time? Does the business require huge amount of debt/equity financing for each additional revenue it generates. You should be very clear on how it achieves operating leverage in the end. Check the quality of sales growth - EBIT growing faster than Rev Growth. SBC is fine, as long as growth rate > dilution rate. Check if FCF/share growing?

✓

The strategic partnership with CBRE and Blackstone - largest real estate services firm in the world gives them a natural pipeline of new customers to allow them to grow their business with minimal S&M costs. This allows them to grow topline disproportionately, with smaller increase in S&M cost.

There is also room for margin expansion if it expands its community solar initiative to the existing portfolio base (at 25% penetration currently). Doing so allows it to sell excess produced power from the generation assets at retail price to retail customers rather than selling it back to the grid at wholesale electricity price.

Lastly, it has optionality in introducing new products such as its energy/carbon management platform AltusIQ which could introduce software like GP margins. Even better is that this product can be charged without high S&M or customer acquisition as it is simply an add-on subscription service to existing customer.

6. Capital Structure

Is it a capital-light business model?

No large fixed costs required to build infrastructure or need for constant R&D to generate revenues. (Eg. Pharma, electricity generation business)

✖

Altus has to take on debt to grow as they have to come up with the construction + lease cost upfront to build the solar cells on the rooftops. They only get paid once the solar systems are up and running and customers pay them for the electricity they consume.

However, the good thing is there is not huge need for S&M and R&D to grow the business as compared to software and tech companies. This is simply a borrow at 4%~ from BX, “loan” to buyers at 10%, lock in 6% margin for 20 years.

The larger the asset base, 6% x a very large number = very high EBIDTA or cash flow to Altus.

7. Category mindshare

Does the business possess a brand that people think of immediately when they think of a service/product (eg. Tesla when people think EV). This is the best form of sustainable advertising without paying for S&M costs.

✖

They are the only pure-play listed C&I listed on the stock exchange. It will probably not have a category mindshare as there are various providers of solar installation company and it all boils down to who can provide a solution/package at the end of the day. Altus is however the market leader in the US in the C&I space and I expect its presence to continue to grow,

They have a huge pipeline of customers that come primarily from their sponsors, and many of the tenants who are currently renting from them have overseas footprint so this mindshare is less important as scaling and growing topline is not a problem.

8. Management

Does CEO have a long range profit outlook - deliberately focusing on quality of its final product/service or is the CEO simply milking its existing success without much vision (short-range thinking) Is the management very clear on its vision of how it will achieve the revenue run rate? Are they good at allocating capital in accretive reinvestment opportunities - either through R&D or acquisitions. Are management incentive aligned to stock performance, CEO/founder own a lot of shares???

✓

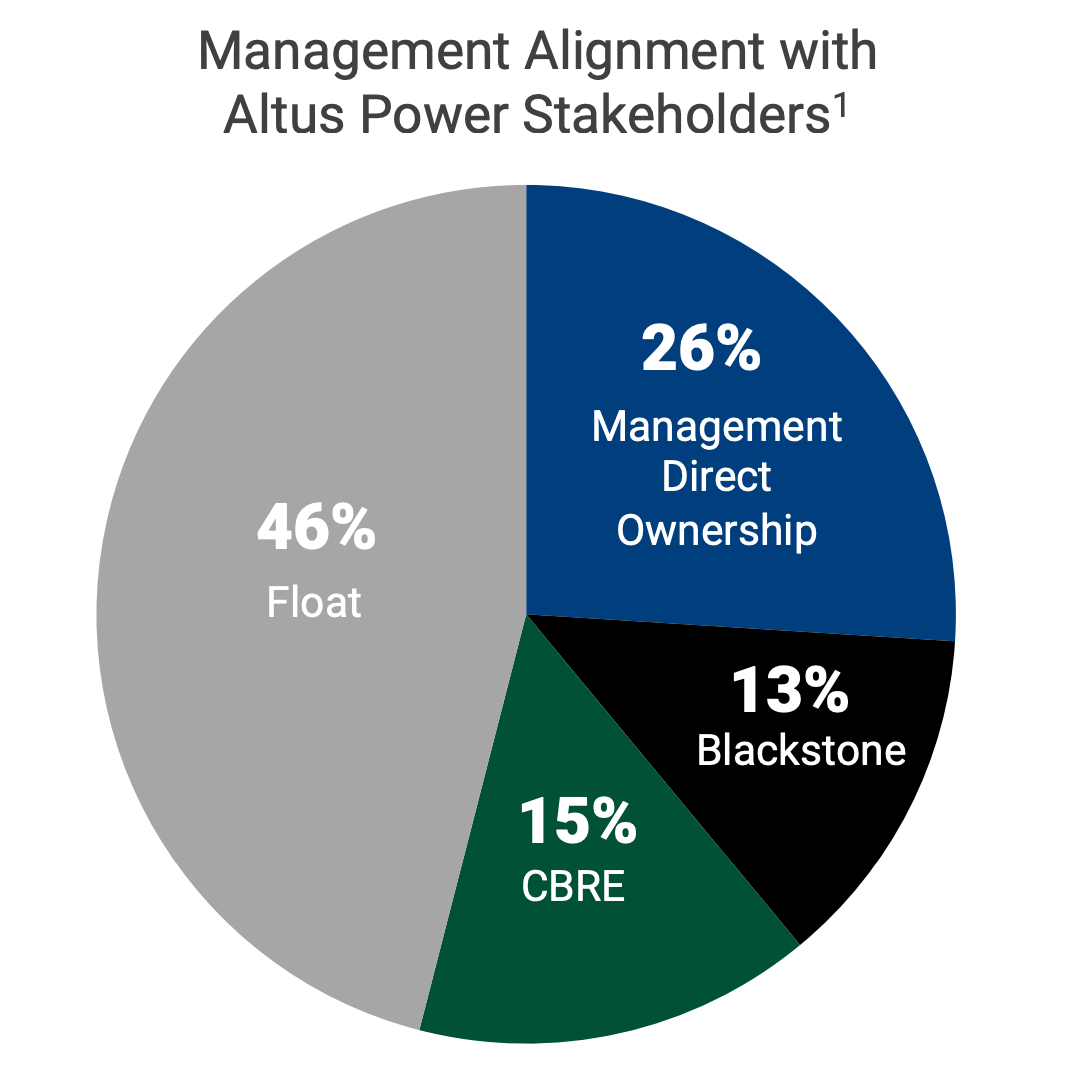

Altus feels more like a private company that is owned by - founding team + Blackstone + CBRE. It is in their incentive to push for Altus’s continued growth with 55% skin in the game between founders and strategic partners.

Note that management has not sold any significant holdings since de-spac days. Greg owns slightly over 10% and Lars owns 2.7%. Of the 46% Float, the significant one is Start Capital LLC which own 15% of shares

9. Stage of business cycle

Is the company in, (1) discovery, (2) acceleration/acceptance, (3) mass adoption, or (4) mature growth?

✓

Altus has just de-SPAC in 2021 and is in its early stage of growth with a current portfolio of 377MW of generation capacity. As mentioned above, the penetration rate for C&I rooftops using solar power is only 5% with a long runway for growth.

I would classify AMPS to be in the middle of the discovery and acceleration/acceptance phase as it slowly adds on generation capacity and expand across all states in the US.